TIPS FOR STRETCHING YOUR DOLLAR

- Make more meals at home and buy things in season and freeze or can it for later.

- Use the food you buy instead of throwing out a bunch.

- Teach your children the value of money and actually make them work for their allowance.

- Get to know your community so you can trade favours with those around you.

WELCOME TO A TIME OF INFLATION, UNCERTAINTY, AND RISING INTEREST RATES

It has been a long time since we have had this much inflation – in fact, the last time was when we had Trudeau Senior in power. History has a funny way of repeating itself, doesn’t it? The Bank of Canada is increasing interest rates to slow the inflation and housing market down and it is beginning to work, but it also means that the massive amount of debt the federal government has taken out lately is about to become very expensive to maintain. People who took out a big mortgage to buy in to the recent housing frenzy are going to be hit with a double whammy as the price of houses fall again and interest rates rise. Supply chain issues still plague the world and now there is talk of potential famine. Things are about to get rough.

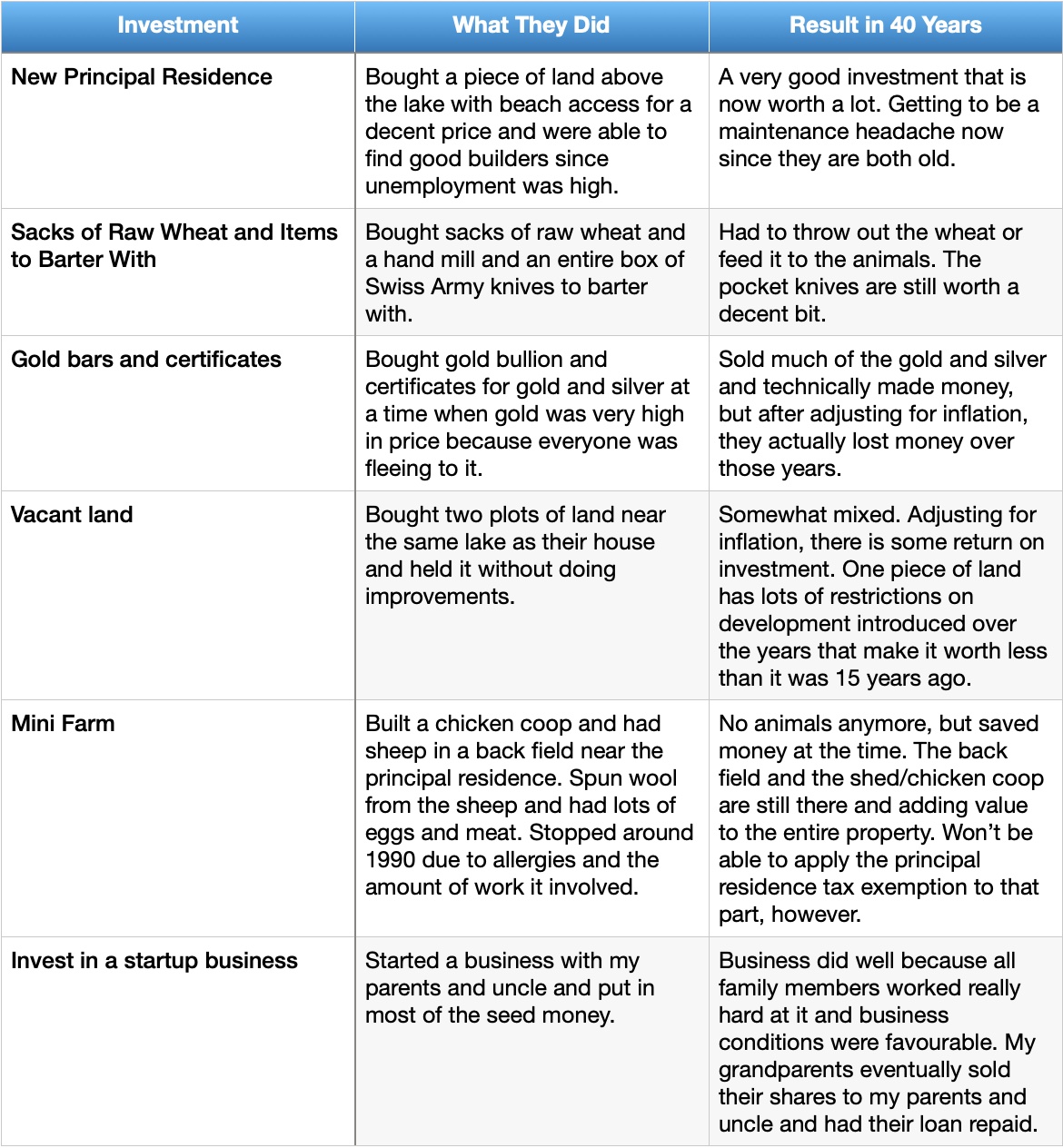

What should you do with your savings in this kind of an environment? Let me give you an example of diversifying wealth in a time of inflation and uncertainty. My grandparents moved to Canada in the late 1970’s. They were lucky in that they brought quite a lot of wealth with them, but when the inflation came, they were also trying to figure out where to put it so that it wouldn’t lose value. Here is a list of what they invested in and what worked out 40 years later and what didn’t.

As you can see, the home was a good investment because the land was a reasonable price and it was a good time to find builders, but our current market isn’t there yet. The vacant land was a mixed bag. The huge sacks of wheat was a panic buy that didn’t end up being needed and the gold was also a panic buy because everyone else was doing it. This time, people aren’t yet fleeing to precious metals and the prices are more reasonable, so it may work out better. Taking up farming was a decent move since it was both a hobby and a source of food and clothing security, but it only really worked because there was the land at a good price to do it. Starting a business was great, but only because they already had the seed money and didn’t need to get a 25% interest rate loan from the bank. In our current environment, interest is still fairly low, so starting a business could be good if you can lock in a longer term loan at the lower interest rates and if you are in an industry where demand will still be high in a recession.

Should you invest in something like cryptocurrency? Probably not. While it is a secure medium of exchange (unless the end user on either side is hacked), it has no asset backing and is only valuable because a bunch of people agree it has value. If you decide to invest in it, please only invest about 5% of your total savings, not 50%. Diversification across different industries, different countries, and different kinds of assets are key. If it is a decision between paying down your mortgage quicker or investing in risky assets with your extra cash, it is wiser to pay down your mortgage as housing will always be essential.

What can you do in your daily life to reduce your living expense and make your money go further? Growing your own food is an option, but there are many other ways to reduce what you spend on food. How much food do you end up throwing out? Do you eat out often or do you make meals at home? Have you learned the art of cooking big meals and freezing portions for a later day when you don’t feel like cooking? Do you buy things in season and on sale and have you learned things like canning and drying fruits? If you buy food in bulk, do you actually use it all or does a large portion get thrown out? Managing your food expense can go a long way. Pets are another potential money pit. Your dog really does not need all that pampering. If you have children, teach them the value of money and pay them according to the money and time they save you; ie. when they do their household chores, walk the dog, and make meals. They shouldn’t get an allowance simply because they live under your roof (heck, after 18, I had to pay my parents rent and there was no allowance).

And finally, let me stress the importance of community. The next few years could be rough, but let’s get out of our COVID isolation mentality and start helping each other out. Practice your bartering skills and learn how to exchange favours with your neighbours. We can get through the rough times by working together.

If you need help managing your cash flow and trimming expenses, feel free to reach out to me for a no-obligation introductory meeting to discuss your situation.