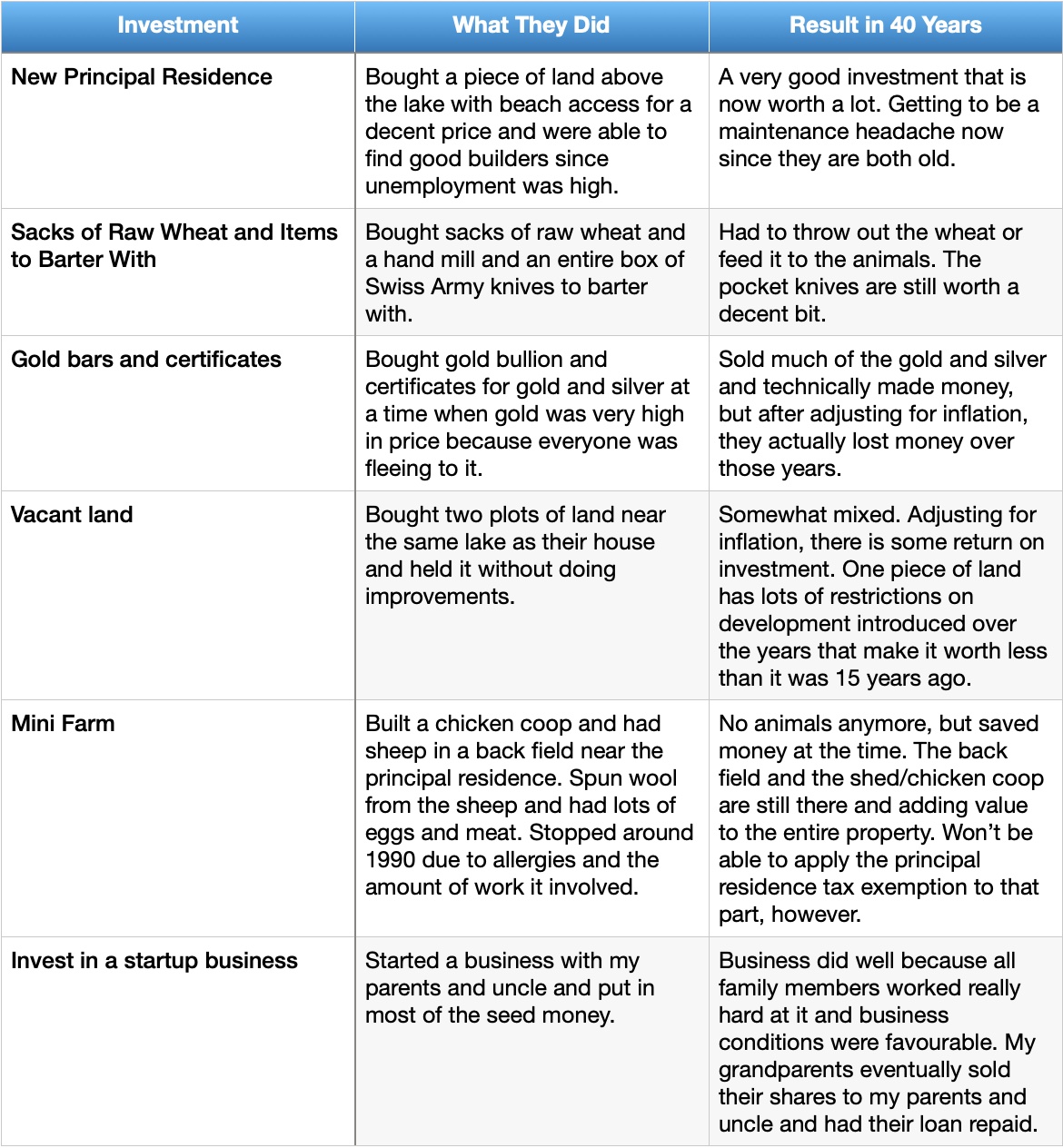

Dishwashing soap bought in 2021 vs same dishwashing soap bought in 2022 on right. A decrease of almost 60 mL for the same price.

If you feel like the stuff you are buying is just not going as far as it used to go, I’m here to tell you that you are not imagining things. I started noticing it in small ways around the grocery store and it is quite subtle. The packaging looks basically the same to the naked eye, but there is less in it than there used to be. This is a phenomenon known as “shrinkflation” and is a way to make people feel like prices are still similar when they are not.

You’ve probably noticed the increase in food prices, particularly staples like meat, eggs, and milk. There have certainly been complaints made about those, but those items aren’t the ones usually subject to shrinkflation because they have standard quantities. It is the shelf items that you will need to watch out for. I suspect that, as a result, prices have increased even more than the inflation numbers the government is currently putting out.

How did we end up with such large inflation? Contrary to popular belief, the government does not create value – it merely redistributes it. Granted, the government has some public utility companies and transportation services that do produce value, but very inefficiently (just ask my brother who worked for BC Hydro). The government has recently been touting it’s success at creating jobs after the pandemic, but upon closer examination, we discover those jobs are mostly government jobs – in other words, those jobs do not create value but just leech money from the sectors of the economy that are actually creating goods and resources. Worse, most government jobs are created to expand some sort of compliance requirement, meaning more paperwork and lost time for the sectors of the economy that are trying to produce value.

Inflation historically has often occurred in countries where the government attempted to print money to buy their way out of a crisis. Germany in the 1920s, Zimbabwe, Brazil, and Argentina to name a few. The inflation sometimes got so bad that the money wasn’t even worth the paper it was printed on and people would go after work and spend their whole paycheque on goods because otherwise their money would lose value overnight. During the recent pandemic, many countries including Canada started printing money to distribute to needy people and sectors of the economy. Problem is, that money was still chasing the same amount of goods produced. Divide the money over the goods available and it means the goods suddenly cost more. Economics 101. Now, the consequences of the government spending are hitting the country and the people will pay for it one way or the other – either through more taxes or higher costs of living. Value cannot simply be summoned out of thin air by government.

The next time a politician promises you a bunch of new programs and spending that are supposed to help you out, remember that they are bribing you with your own money.