Giving Your Kids Money Now vs Later

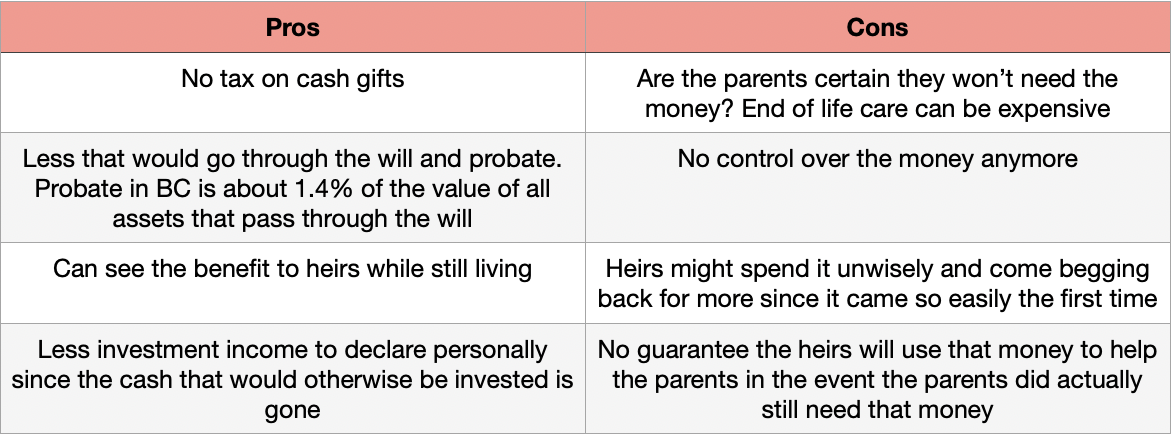

Many elderly parents are downsizing their homes, simplifying their affairs, and getting their estate planning done. Often they end up with extra cash from liquidating property that they feel they likely won’t require for their lifetime and the question arises whether they should give some of it to their heirs now instead of later. There isn’t really a right or wrong answer to this question. As long as the parent isn’t giving away property with unrealized gains and is just giving cash, there are no tax consequences in Canada. In fact, it may even help save future tax and administrative costs. However, there are non-financial reasons why giving away money now may not be the best idea. The below is a chart of some of the pros and cons of giving an advance on the inheritance.

If parents do want to go ahead and gift some of their money while living, how do they make sure that each child is treated fairly? Some children might be begging for money now while others are doing just fine financially.

Let me give you some suggestions for how to give an advance while keeping things equal and fair between all the children.

#1 – Make it a Loan Instead of a Gift

Instead of making it an outright gift of money, give a loan to those children who are in need of money now and make it official. That’s right – get a lawyer to put it on paper and have it properly signed with interest and repayment terms. If no repayment is required or if there is a balance still outstanding when the parents die, then it must be deducted against that child’s share of the inheritance in order to keep things fair for the other children. Loan balances should be carefully maintained and kept with the will documents. There have been many estate disputes in the courts where one child claims there was a loan to another child and that child claims it was a gift. Without documentation, it is basically one person’s word against the other.

I would also recommend setting an interest rate at least equal to inflation on the loan, even though this ends up creating some income for the parents. This ensures there isn’t a benefit for the children who got money immediately compared to the children who waited.

#2 – Set Money Aside for Children Who Did Not Receive an Advance

In BC, if the will does not distribute the estate equally to all children, the children can use the wills variation act to try and get a better result. It is highly recommended to treat all children equally in the will. So how can parents make sure that children who did not receive an advance on the inheritance get extra in the estate to make up for not receiving any earlier?

A simple solution would be to put that money aside in segregated funds for the children who did not receive any money up front. A segregated fund is available through insurance companies in Canada and allows beneficiaries to be named on an account so that the money goes straight to them instead of passing through the will. While usually beneficiaries can only be named on retirement accounts like a RRIF or on a TFSA account, segregated funds can have beneficiaries named even on non-registered accounts, making it ideal for proceeds arising from the sale of a home. Because it does not pass through the will, it is not subject to probate and the wills variation act and it is entirely confidential. The segregated fund will earn an investment return on the money in it, making up for the time value of money that the children who received the money up front got. Money is not locked in to a segregated fund (unlike annuities) and the parents can still withdraw money if they need it.

For instance, let’s say an elderly couple sells a home for $1 million. They keep $500,000 for themselves, but feel that they can afford to give the rest of the proceeds to their four children. Of the four children, two are quite eager to have the money now, but the other two are financially stable and don’t need it immediately. If they give $125,000 to each child that needs it now, then they should put $125,000 for each of the other children into a segregated fund where that child will be the beneficiary upon the parents’ passing. If the investments in the segregated fund do particularly well, the parents can withdraw some of the funds for themselves while they are still living and leave the rest for the children. This is because segregated funds can hold mutual funds much like regular investing, so it is likely that it will return more than is needed to make up for inflation.

At the end of the day, estate and inheritance planning is not simply about having a will in place. The will only deals with the assets that actually need to go through the legal process of probate, but anything that is in joint title or has beneficiaries named will bypass the will and the legal estate and must be planned for separately. This is why it is important to have advice both on the legal side for the will itself, but also on the financial side for the accounts and insurance products that can bypass the will. Speak with me for a free consultation to discuss estate planning and the issues that are relevant to your family situation.