Being Incorporated vs Self-Employed

Let’s say you start a small business. One of the first questions people often have is whether to incorporate their business because they have heard that incorporation can defer taxes and shield the owner from creditors who might sue the business. While this is true in most cases, the benefits of incorporation depend largely on the profits made by the business and being incorporated won’t necessarily shield the owner from liability if a lawsuit is due to the owner’s personal negligence. So when should you consider incorporation?

First, you need to consider the type of business you are in. A lot of larger businesses like to hire contractors because it is much simpler than having an employee and the contract can be easily terminated after the project is finished. If your business is mainly sub-contracting your skills out to larger companies, then you need to be working for multiple companies in a year, otherwise CRA will consider you to be a glorified employee. They may also chase the business who sub-contracted to you for employee remittances because they should have just hired you as an employee. To be properly sub-contracted, you need to have your own tools for the work, show that your hours are based more on deadlines for the project than the business’ usual office hours, show that there is an expected end date to the contract, and that you are available and taking contracts from other businesses.

An incorporated small business is a separate legal entity from its owner and that means that it files a separate tax return and separate financials from the owner every year. This is a significant additional cost, so the amount of deferred profit in the company and resulting tax savings must be worth that cost. Also, the incorporated small business must not be treated as the owner’s personal bank. Anything that the company pays for that is used personally must be declared as either salary or a dividend to the owner and taxed in the owner’s hands. This is an area that CRA particularly likes to audit and the penalties are steep.

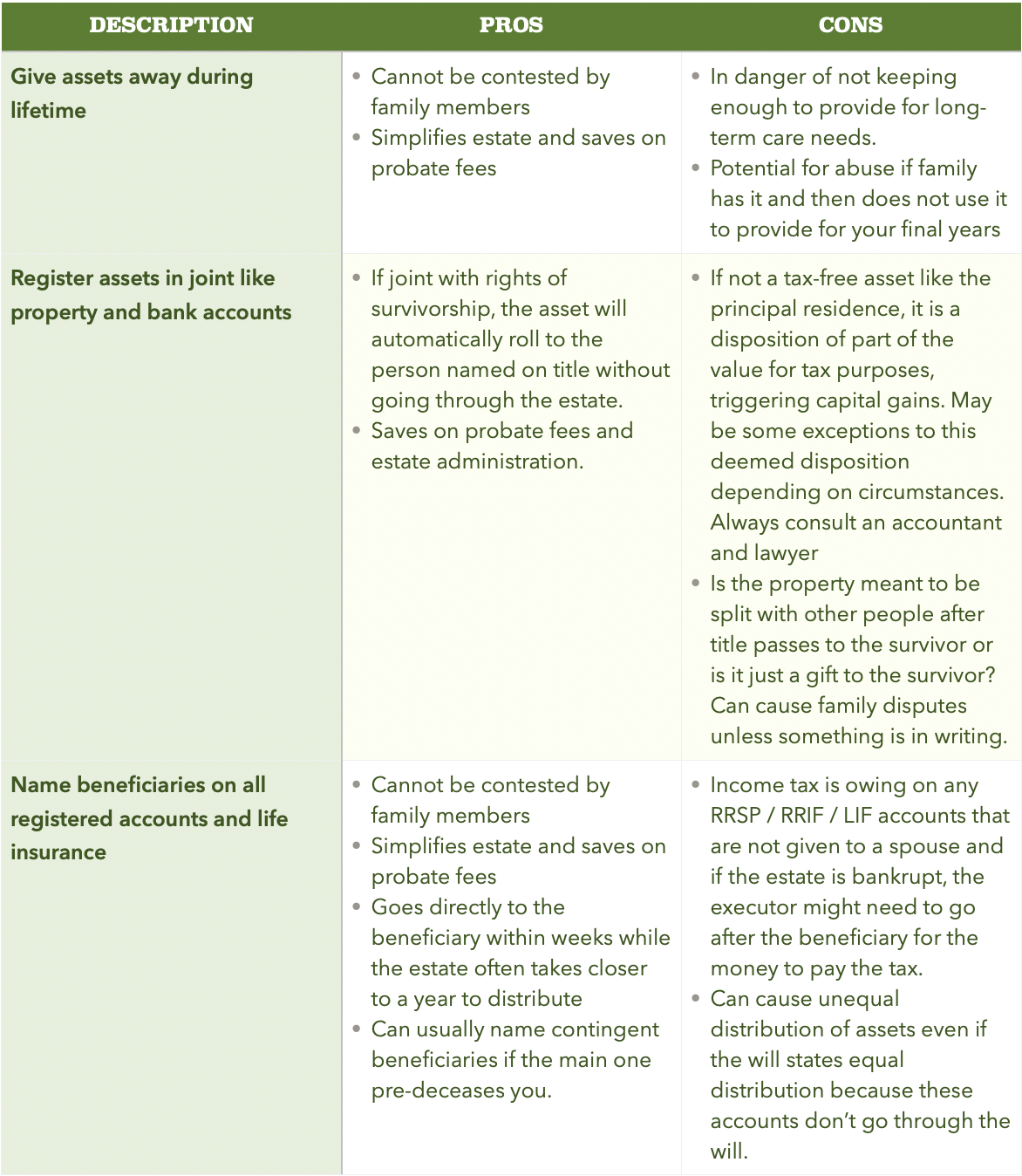

The following table is a comparison of some differences between being incorporated and being self-employed.

There are many things to weigh in the decision whether to incorporate or not and much of it depends on personal circumstances. Please reach out for an appointment if you would like to discuss your own business.